The cost of owning a car (and how to save thousands)

We explain how to calculate your cars running costs. You need to include fixed expenses & the variable cost per km to run a car. All explained here!

How to easily calculate your car's running costs

We all know that owning a car isn’t cheap – as if the initial purchase price weren’t bad enough, you then have registration, insurance, fuel and servicing bills to pay every year. It doesn’t take long for it to all add up to a pretty hefty sum. But do you know exactly how hefty that sum is?

If you only drive once a week to pick up some groceries, your supermarket run could be costing you over $100.

(And that doesn't even include the bread and milk.)

Don't believe me? Let's do the maths and find out for sure.

To really understand how much your car is costing, you need to account for your car’s standing costs, as well as its running costs.

Standing costs are the fixed expenses you have for your car, regardless of how often your drive your car – things like:

- registration;

- insurance;

- interest on your car loan; and

- depreciation.

Running costs are the expenses you incur as a result of actually driving your car – like:

- fuel;

- tyre wear; and

- servicing and wear and tear.

Often when we think about te cost of running a car - whether we're using our own car or lending it to a friend - we only take into account the fuel costs. Which makes it feel like your Saturday trip to the supermarket is pretty much free, except maybe for a few bucks' worth of petrol. Right?

Not quite. Let's get under the hood and find out what it really costs to own and run a car.

Calculating your car’s costs

To work out what your car's running costs are, it’s best to start with your standing costs as these are the same whether you drive every day or hardly ever.

The figures below are based on data from RACV and Vicroads for the cost of buying and running a new Toyota Corolla over 5 years*. To do the calculations for your car, just substitute the figures with your actual costs.

Standing costs for your car

| Cost | Annually | Monthly | Weekly |

|---|---|---|---|

| Registration and CTP insurance | $800.80 | $66.73 | $9.53 |

| Comprehensive insurance | $1,033 | $86.08 | $21.52 |

| Roadside assistance | $105 | $8.75 | $2.19 |

| Interest | $903.84 | $75.32 | $18.83 |

| Depreciation | $2,778.80 | $231.56 | $57.89 |

| Total standing costs | $5621.44 | $468.45 | $117.11 |

Running costs for your car

Running costs need to be calculated on a per kilometre basis.

| Fuel | 7.55c/km |

|---|---|

| Tyres | .68c/km |

| Servicing | 7.18c/km |

| Total running costs | 15.41c/km |

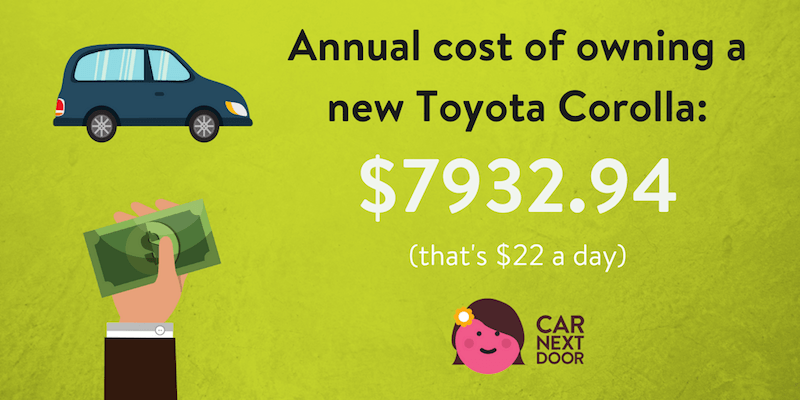

This means your new Corolla is costing you $7932.94 a year.

Even if you hardly ever drive your car, it’s costing you over $5600 a year just to have it sitting around.

And that Saturday trip to the shops?

When you take into account your car’s weekly standing costs as well as the running costs to get there and back, your weekly drive could be setting you back nearly $120.

Yikes.

But I didn’t buy a new car!

I know what you’re thinking: everyone knows new cars are a money sink and that’s why you bought a used car instead.

That was a good move, but the sad fact is that owning a car is expensive, regardless of its age. Let’s look at the annual standing costs for a 2012 Toyota Corolla, bought second hand for $13,488 in 2018*.

| Cost | Annually | Monthly | Weekly |

|---|---|---|---|

| Registration and CTP insurance | $800.80 | $66.73 | $9.53 |

| Comprehensive insurance | $1,119 | $93.25 | $23.31 |

| Roadside assistance | $105 | $8.75 | $2.19 |

| Interest | $444.34 | $37 | $9.25 |

| Depreciation | $1,769.40 | $147.45 | $36.86 |

| Total standing costs | $4238.54 | $353.21 | $88.30 |

7 ways to cut your car costs

Thankfully there are a few ways you can claw back some of these expenses.

1: Avoid buying a brand new car

If you’re currently in the market for a new car, try to resist the allure of the shiny brand new model in the showroom. New cars lose their value really quickly: as you can see in the example above, a used car depreciates at a much slower rate than a brand new model. Get a good deal on an older, well-maintained car and you’ll fare better when the time comes to trade it in or sell it on.

2: Don’t delay on your repayments

Repaying your car loan ahead of schedule will stand you in good stead in the long term. If you can afford to pay more off your loan each month, seriously consider this option as you’ll end up shelling out far less overall.

3: Shop around for insurance

Are you sure you’re getting the best insurance deal? Spend a little time getting quotes from three or four different insurance providers and see how they compare with your current bill. This research shouldn’t take more than an hour but could end up saving you hundreds of dollars a year. Make sure you consider all the factors that contribute to cheaper comprehensive insurance to get the right deal.

4: Save on cleaning by taking care of it yourself

You can get some good deals on a prefessional car clean, but it really doesn't take long to do it yourself. In fact, you can do it home with these car detailing tips. You'll just need to invest in a few good quality car cleaning products. ALternatively you can give your car a prety good clean for just a few dollars at your local hand car wash.

5: Strive for fuel efficiency

Fuel costs fluctuate from day to day, but there are some simple things you can do to make your tank last as many kilometres as possible. Maintaining your car’s recommended tyre pressure and not carrying around unnecessary clutter in your boot will keep your engine running to maximum efficiency. A lesser-known tip is to get fuel efficient tyres. The next time you need a new set – this could shave up to 10% off your fuel costs.

6: Keep your tyres in good condition

Replacing your tyres can be really expensive, but there are some simple things you can do to keep them lasting as long as possible: check your tyre read regularly, keep them out of the sun, and keep them aligned correctly to extend their lifespan. Learn more about how to make your tyres last longer

7: Put your car to work

If your car is like most cars in Australia, it probably sits idle for about 97% of the time. When you consider how much you’re paying to keep your car sitting around doing nothing like that, it really hurts doesn’t it?

The good news is that you can make the most of your car’s free time and get it earning its keep. The two main ways to make money from your car are to drive for Uber or another ridesharing service , and to rent your car out.

To drive for Uber, you’ll need to have a car that’s no more than 10 years old, be at least 21 years old, have an unrestricted licence and be listed as an insured driver for your car. How much money you’ll make depends on your location, the times you’re available to drive and your car’s running costs.

As long as your car is in decent condition, a good location and you’re willing to do a little housekeeping, you can rent it out when you aren’t using it yourself. There are a few different options for renting your car out in Australia: Uber Carshare, Carhood and DriveMyCar. Each operate slightly differently so it’s important to consider which will work best for you.

Uber Carshare allows you to rent out your car when you aren’t using it to a community of approved and trusted borrowers.

You’ll earn money for the time your car is rented, and the distance borrowers drive. For every kilometre a borrower drives in your car, you’ll be paid your chosen distance rate. This would more than the cover the 15.41c/km running costs of the Toyota Corolla above, leaving a little extra in the kitty to cover your own driving.

You set your own hourly and daily rates, with this income going a long way towards offsetting your car's standing costs. In fact, the average owner makes around $3,500 a year, drastically reducing the cost of owning a car.

Joy rents out her silver Yaris in Sydney and loves meeting people in her community. “Renting my car out is a great way to meet local people. It feels good to give back to the community.” For Angie, renting her car out gets it paying for itself. “I much prefer having my car out and about earning money for me than costing me money!”

Renting your car is pretty easy and doesn’t take too much time. If you want to give it a red hot go, there are a few things you need do to maximise your earnings: keep your car’s calendar up to date, keep your car clean, and be proactive in contacting your borrowers before and after each booking.

Sharing your car with your neighbours is an easy way to earn passive income and get your car paying for itself. And with every share car taking up to 10 individual cars off the road, you’ll be helping your community and the environment as well.

*Cost assumptions

- Registration and CTP insurance: quoted on Vicroads website for a small car's annual registration/CTP fee (March 2018) Initial purchase price (new car): based on figures from RACV

- Initial purchase price (used car): based on advertised price for a 2012 Totyota Corolla on carsales.com.au (March 2018)

- Registration and CTP insurance: quoted on Vicroads website for a small car's annual registration/CTP fee (March 2018)

- Comprehensive insurance: quoted by RACV for a 2018 Toyota Corolla, with the youngest driver a 30 year-oldmale (March 2018)

- Roadside assistance: price quoted for RACV Roadside Care for a Blue member (March 2018)

- Interest (new car): based on figures from RACV

- Interest (used car): quoted by RACV, borrowing the full initial purchase price, with monthly repayments over 5 years, for an RACV Blue member (March 2018)

- Depreciation (new car): based on figures from RACV

- Depreciation (used car): average annual loss of value over five years based on figures from the ATO’s depreciation and capital allowances tool

- Running costs: based on figures from RACV*

){kind=link}